Juan Manuel Pico

Publicado originalmente en

In this challenging scenario, governments around the world need to prepare strategies to mitigate the damage and be more prepared for the future to come, especially in two areas: to address potential barriers to student engagement by providing adequate technological and infrastructure resources, such as free internet zones, plus laptops, tablets and even low-cost smartphones, along with skill development programs (without them it could only be a sterile move); and to provide personalized support to students, by understanding that every student has its own dynamic and its own pace of learning, what we could call massive personalization.

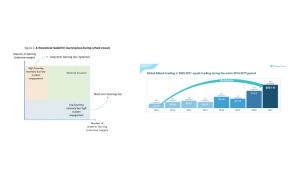

In 2019, the OECD published a “Theoretical model for learning loss during school closure” as part of the report PISA 2018 Results (Volume II): Where All Students Can Succeed, where the potential learning loss is the effect of two concurring factors: how much students have learned during school closures (the “intensive margin”) and, on the other hand, how many students have continued to learn during the school closures (the “extensive margin”). As the graphic shows, a high learning intensity but a low student engagement leads to what the OECD calls long-term learning loss or hysteresis, a term used in labor economics that refers to the long-term effect of unemployment on a worker´s ability to find a job. Transferred to the education landscape, it refers to the long-term impact of school closures on students’ outcomes.

The hysteresis moment where we are at drives us to extremely difficult consequences: students struggle to maintain their learning pace due to their lack of practice; high challenges in re-engaging with education activities and their demotivation as they feel they are falling behind from where they should be standing today. This is particularly critical in Latin America since internet infrastructure and IT resources are scarce among students from underprivileged areas.

In order for our students to flourish in such a post-pandemic situation, governments in the region are not the only ones to be part of the solution. Hopefully, before the COVID-19 arrived, the world had seen a double trend in EdTech: from one side, a proliferation of EdTech startups proposing all sorts of solutions to be implemented at the classroom, helping students to learn faster and retain more course material than traditional teaching methods, giving them the possibility to be engaged with activities they like thanks to the adaptive learning tools embedded within the EdTech platforms; and on the other side, funding availability like never before, as a result of the appetite of investors to look for new lines of investments beyond FinTech and E-CommerceTech industries. The numbers speak for themselves.

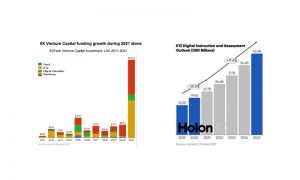

According to The European EdTech Funding Report 2022 from Brighteye Ventures in London, the combined global EdTech funding figures for the two-year period of 2020-2021 equal funding secured during the entire six-year period of 2014-2019, yielding to a 6-times growth in funding from 2014 and 2021, reflecting a dynamism and a vibrant ecosystem that is maturing.

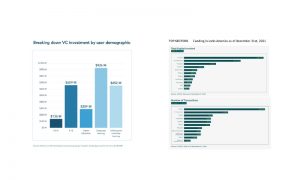

A breakdown Venture Capital investment by user demographic for Europe shows that despite corporate learning is the biggest destination for investment (35%), K12 remains second (25%), as a result of the pandemic, where increasing adoption is being created to support traditional K12 education, rather than replace it. The hysteresis moment has started to be fixed, and the DeLorean car has come back from 2030 with solutions at hand.

HolonIQ, a global market intelligence firm from Australia that oversees the global learning landscape, has forecasted that the global K12 digital instruction and assessment market will reach USD$42.5 billion by 2025, “accelerated by the sudden shift to remote learning through COVID, where educators, children and their parents have embraced technology like never before”.

A similar trend, but with lower numbers, is happening in Latin America. The EdTech venture capital activity tracked from 2011 is gaining momentum and has reached USD$1,07 billion of EdTech funding for the last 10 years combined, where 2021 alone has represented 46% of the total investment amount in a decade, and 6 times the investment value from 2020.

As it is happening in Europe, Workforce Solutions and K12 are the two most relevant EdTech sectors that are receiving major investments as it is shown in the graphic, calculated by HolonIQ. However, the trends in the region are slightly different. Europe and the United States are more mature in terms of K12 EdTech adoption, while Latin America is way behind, probably due to the fact of not being early adopters for EdTech solutions at schools. Traditionally, the public school system in Latin America has not the willingness to hardly invest in technology. Thanks to the COVID-19 things are starting to change dramatically, where the word digital is now beginning to be present in the public agenda. On top of it, Latin America is witnessing a proliferation of local venture capital funds who are investing. In the past, if you wanted to reach a venture capital fund you needed to take a flight right up to Silicon Valley. Today, and especially during the last three years, things have changed to the better.

According to LAVCA (The Association for Private Capital Investment in Latin America), venture investment reached USD$15.7 billion in 2021, more than 3 times the previous record of USD$4.9 billion in 2019, and more than the previous 10 years of venture investment combined. The fact is that fresh funding money has landed in Latin America and the trend will continue as the years go by. There is a remaining challenge, which makes the difference with the United States and Europe, since the money flow has been going mainly to FinTech, E-Commerce and PropTech. Surprisingly, in number of transactions as of December 31st, 2021, EdTech came third after FinTech and E-Commerce, which shows that Pandemic has sent its urgency message even to investors, but there is still a long way to go in improving a more mature process of investing in this sector.

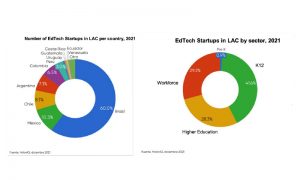

We can say today that Latin America is having a “renaissance” in terms of entrepreneurs focused on all type of EdTech solutions. EdTech is starting to be part of this new wave of rising starts, especially because the education problem at stake has a monumental dimension, and now it does not depend exclusively on governments. It is something where parents, private sector, and investors are also involved. According to HolonIQ, 35% of EdTech startups in Latin America have less than five years old, and 12% started their endeavor in 2019 or 2020.

Within the region, Brazil is leading the way, making up just over 60% of the EdTech startup list, followed by Mexico, Chile, Argentina, and Colombia. In terms of topic focused, K12 is now leading the way (41,6%), followed by Workforce Learning, and Management Systems, that make up almost one third of the numbers, as this is an area that remains strategic for governments, employers, and individuals. K12 has finally risen as a natural consequence of what has happened with the Covid-19 during the last two years, and it is just the beginning.

The digital era is here to stay. The pandemic accelerated the education needs in terms of closing the digital divide like never before. Venture capital investors are increasing its presence monthly. These are global and local signs of a new era, a moment of “education renaissance”, where technology is a main actor, educated and bold entrepreneurs are at the rise, investors are trusting the convergence between technology and education as they have been doing with Fintech and E-commerce. Probably, we needed a universal crisis to have a fresh look at education, that had remained untouched during the last 200 years. Latin America finally is witnessing EdTech solutions that are betting to speed up the quality of education, the personalized massification, and the adaptive learning, where every child is unique and every child, no matter what, counts and deserves to receive the best available learning opportunity. Welcome to the beginning of a new era.